How to make Joe Biden’s child benefit even better

Days before his inauguration, President Biden unveiled the American Rescue Plan, a $1.9 trillion package to combat the COVID-19 pandemic and provide relief to American families. The plan includes a significant expansion of the Child Tax Credit, one of the country’s largest financial benefits for families with children.

This would provide meaningful aid to many American families, particularly those with low incomes. But it could be made even more effective if Biden goes a step further and converts the annual tax credit into a monthly direct payment to support families year-round.

The CTC currently reduces some families’ tax liability by up to $2,000 per child. Biden’s Rescue Plan would increase this in 2021 to a maximum of $3,600 per child under six years old, and $3,000 for those under age 18. (The CTC’s benefits gradually phase out for upper-income families.) Importantly, Biden would fix a longstanding shortcoming of the CTC to allow the poorest families to reap its full value. Currently, families who earn too little to have much federal tax liability get only minor benefits from the CTC, and the poorest of the poor are excluded from the CTC entirely. Biden’s plan would correct this unequal treatment by making the CTC fully refundable for all families.

Another issue remains unresolved: how and when to deliver the juiced-up CTC to families. Because it is submerged in the tax code, the child benefit has historically been distributed once a year during tax season. Continuing the status quo would mean that families would garner no benefit from an expanded CTC until the spring of 2022 — an oddity in a package designed to provide immediate pandemic relief.

Biden’s team seems unlikely to wait that long, and is reportedly still weighing its options on how to get benefits out to families faster. Commentators like The Atlantic’s Derek Thompson are urging the administration to “replac[e] the child tax credit with a universal child allowance.”

That would be ideal — a simple direct-checks, Social-Security-for-the-young approach would be the policy that achieves the “maximally awesome,” as Thompson puts it. But as a second-best option, Biden could likely craft a work-around using the CTC to approximate a child allowance. Rather than making everyone wait until filing taxes next year, the best way to maximize the impact of the expanded CTC is to pay it out in advance to families through monthly checks of up to $300 per child.

Getting the most bang for the buck

Advance monthly checks would simply be worth more to families than a once-a-year reduction in their tax liability. Monthly checks would avoid the siphoning problem that currently plagues the CTC and other tax credits targeted toward working families (including the Earned Income Tax Credit). Families today face the obstacle of having to file federal taxes to access the child benefit at all, even if they aren’t otherwise obligated to file taxes. Most low-income families rely on for-profit tax prep services like H&R Block or TurboTax. They pay fees to have their taxes prepared and filed, which offsets some of the value of the CTC. And many of these companies have pushed low-income filers toward high-fee “refund anticipation checks.” The private sector is thus filling a gap left by government policy while capturing a slice of the tax benefits meant to aid those in need of financial help.

Those families who go it alone without a tax preparer risk missing out on child benefits and other credits to which they are entitled. IRS data shows that only 78 percent of families eligible for the EITC actually receive it.

The CTC’s value also currently gets diluted by its once-a-year payment structure. In their 2015 study of low-income families It’s Not Like I’m Poor, researchers Sarah Halpern-Meekin, Laura Tach, Kathryn Edin, and Jennifer Sykes found that families are forced into a boom-and-bust cycle, where they scrape by most of the year until they claim benefits like the EITC and CTC during tax season. For these families, “[g]etting into debt and trying to dig out of it were near-universal experiences.” One study found that 84 percent of families receiving the EITC fork over some of their refund to pay down debt and overdue bills.

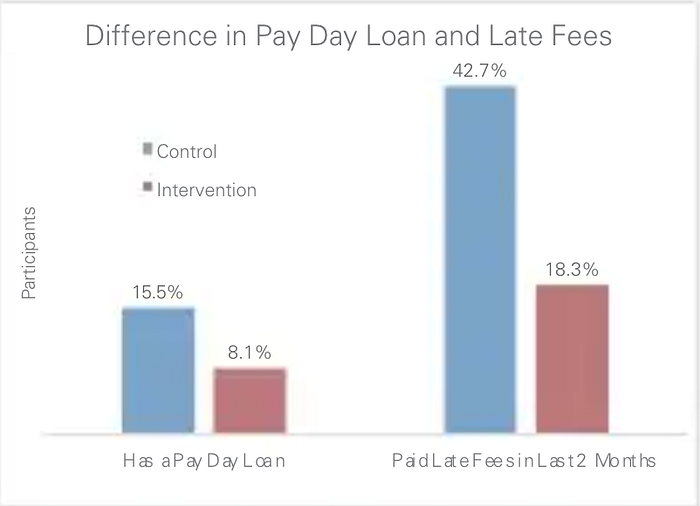

Paying out the government’s family benefits throughout the year instead of as an annual lump-sum refund would smooth the budgets for these families and spare them from predatory lenders and costly bank overdraft fees. In a 2014 experiment, more than 300 families received half of their anticipated EITC refund over four quarterly payments. (For instance, a family that received a $2,000 refund the previous tax year got a $250 check every three months, and the rest as a regular tax refund.) Not surprisingly, the study found that families receiving quarterly checks experienced improved financial stability, stress levels, and overall mental health. Advance-check recipients (the Intervention group in the chart below) were also able to build savings, reduce their reliance on payday loans, and pay far fewer late fees in comparison to participants who did not receive advance checks (the Control group):

The upshot is that by withholding tax credits until filing season, the government forces families into debt and inflicts financial and emotional stress upon them. By delivering child benefits throughout the year, we could ensure that families themselves get all of the resources they are owed when they need them most.

We can do it

There is precedent for providing advance direct payments of child tax benefits. The 2003 Bush tax cuts increased the CTC by $400, which Congress paid out in advance to eligible families through checks from the IRS in order to provide immediate benefits to jumpstart the economy. Stimulus legislation in 2008 included a one-off child allowance that mailed a $300 per child “recovery rebate” to families, structured as a top-off on the CTC.

This structure has been used in other contexts too. The Affordable Care Act’s subsidies for people purchasing individual health insurance plans are also structured as tax credits for insurance premiums, which are paid out in advance.

While using a tax credit to provide immediate relief to families poses some logistical complexity, these examples show that it would be technically feasible to do it again now. The 2003 Advance Child Tax Credit is illustrative. To execute that program, the IRS automatically mailed checks directly to any family that claimed the CTC on their 2002 tax returns. Families did not need to reapply or submit any kind of additional tax filing to access the Advance CTC. And the IRS tolerated overpayment: families who had income changes that caused them to receive a larger Advance CTC than they were actually owed did not have to repay the advance when they filed their 2003 taxes.

Based on that model, Biden’s expanded CTC could be structured with a similar design. Eligibility for advance payments could by default be determined based on last year’s income, so monthly checks could automatically be mailed out to anyone who claimed or could have claimed the CTC in 2020. And for the sake of administrative ease, we’d tolerate overpayment to families who, for example, saw their incomes jump from 2020 to 2021 and may no longer be strictly eligible for the amount of the CTC they receive in advance.

At the same time, we’d want to make sure the benefit is reactive to family and income changes. Millions of people have lost a job, lost income, or had children since they filed their 2020 taxes. So we’d want to have a mechanism for those families to receive a monthly CTC advance. They should be able to file a simple certification with the IRS attesting to their changed income and/or family size, allowing them to begin receiving the advance CTC. (We offer something similar for federal income-driven student loan repayment: borrowers can file a relatively simple certification at any time to have their monthly payments recalculated if their income drops.)

That option should also be available to families who did not file taxes last year but are eligible for the revamped CTC. And we’d especially want the government to initiate affirmative outreach to those non-filers and the estimated one-in-five families eligible for the CTC who nevertheless do not claim it to make sure they get their benefits. If needed, this outreach could look like a smaller-scale version of the outreach, advertising, and navigator support that accompanied the Affordable Care Act to help people access their new healthcare benefits.

This is all avoidably complex in comparison to a simple universal child benefit mailed out to everyone by the Social Security Administration. But if political constraints dictate that we continue using the tax credit structure to pay out child benefits, this design will help to more closely approximate the ideal policy.

Making it even better

Biden’s expanded pandemic CTC is based on the American Family Act, which would make monthly family assistance checks permanent, and which 38 Senate Democrats have sponsored. One of that bill’s lead sponsors, Senator Sherrod Brown (D-Ohio), has discussed with Treasury Secretary nominee Janet Yellen the possibility of depositing child benefits directly in new bank accounts run by the Federal Reserve for all Americans. “The $250 a month will go to these low-income families every month, year-round — $300 if your child is under five,” Brown said. “Why not have this directly deposited in one of these Fed accounts everybody can have? Just imagine the difference it would make for families who are struggling.”

Imagine indeed. Experts estimate that these monthly checks would cut the child poverty rate in half, rescuing 5.3 million children from poverty. In a pandemic, monthly checks for some families could mean the ability to stay current on rent, put food on the table, and keep the wifi active so their kids can participate in remote schooling. Seamless instantaneous delivery into a FedAccount synced up to your Social Security number would get money to families even faster, avoiding disruptions like mail delays or missing direct deposit information.

Biden has the right idea to boost the support we provide to families with children. He should deliver that support on a monthly basis so families in need can make the most of it.